I’ve been writing about something that has become a regular part of my life: volunteering. I started regularly volunteering in 2024. I’ve been thinking about the reasons I volunteer — and I have found that there are some not so obvious benefits that volunteering provides. Instead of sharing all of my ideas at once, I’ve been sharing a few at at time. (Less pressure!) Following that approach, here are reasons 6 and 7.

A description of the feature image is at the end of the post.

Reason 6: Volunteering is kryptonite for your haters

We all have our haters. I’m willing to admit it. You know you do. And I’m sure there are people out there, right now, who could list off at least 5 things they dislike about you. Some grudge they’ve been holding onto for years….

Maybe in the past you might have internalized this hate and asked yourself…am I a bad person? The answer is: NO! As long as you’re volunteering, you get to say, with the type of documented evidence employers say they love to see on a resume, that you are NOT a bad person. You volunteer at senior homes. You deliver Meals on Wheels. You are not a bad person.

Are you still flawed and imperfect? Yes, most definitely. But a bad person? No.

Not anymore, haters!!

Reason 7: Am I…✨better than everyone?✨

Do you play BINGO with seniors or deliver food to home-bound seniors?

Do you volunteer at soup kitchens or support the food insecure?

Do you volunteer with the physically or cognitively disabled?

Do you volunteer with children?

Do you do park clean-ups, urban farming, or something similar?

If the answer to any of these questions is yes, you might be…✨better✨ than everyone else.*tucks hair behind ears*

Sometimes I think this perspective is a little bit selfish and pretentious but, if you volunteer, I think you might be a little bit entitled to ask this question of yourself and answer in the affirmative.

Sleepy young goat on a picnic tableTwo chickens in a chicken coopThe goats fell asleep on a picnic table

I admit, both reasons 6 and 7 might be THE main, “selfish” reasons to volunteer. No matter what else you’re doing in life, being able to say to yourself, “I deliver Meals on Wheels” really makes you feel like…maybe you’re…✨better✨.

I was remembering some disagreements with someone in my past. I can come back and say to them: I am not a bad person. No one who does as much volunteering as I do, doing the activities I do, helping people as much as I do…. Nope! You cannot accuse someone who does all that of being a bad person.

So if you were looking for any kind of ammunition against haters and negative self-talk volunteering might be your way to go.

The images for this post are from a project where volunteers cared for chickens and goats. The featured image includes a hen on some shelves. She was apparently trying to “brood” or become a mother. But there were no roosters, so that wasn’t going to happen. The goats were dairy goats about 4-6 months at the time. As for the chickens, we cleaned a lot of poop and we got to collect eggs.

I’ve been regularly volunteering and I’ve decided to share some of the not so obvious benefits. In this second post, I talk about experiencing new activities.

Introduction

As I wrote about in my first post on this topic, I’ve decided to write about something that has become a regular part of my life: volunteering. I started regularly volunteering in 2024.

I am writing about this because I’ve been thinking about the reasons I volunteer — and I have found that there are some not so obvious benefits that volunteering provides.

Instead of sharing all of my ideas at once, I’m sharing a few at at time. (Less pressure!) Following that, here are reasons 3-5: Getting to see the city, Finding something to do, and Exploring a range of activities.

Reason 3: Getting to see the city

This might be specific to New York, but as I just mentioned, I like to pick activities all over the city. I get to see new streets and neighborhoods I may have never been to before, or maybe just a place I would walk right on by. Sometimes I go to neighborhoods I moved away from and it’s interesting to see what’s changed. So, if you’re into urban exploration, that’s a benefit.

Reason 4: Don’t just sit there! Finding something to do…

Sometimes I’ve gotten up and I’ve been so surprised that suddenly 5 or 10 years have gone by and I don’t know how that happened.

Or maybe I want to meet up with friends, but they’re all busy and have other things going on. Or maybe I wasn’t invited to a party and feel left out. And even just being introverted…not feeling like I even need to get out.

Volunteering gives me an activity I can plan ahead for and it’s all my own. I like that I can make plans for an activity weeks ahead of time. It feels good to know I have something I can look forward to. Now I’m the one with the plans. And…it’s free!

Reason 5: Explore a range of activities

I may be unusual from some of the other volunteers because I like to rotate the type of activities I do. From my small talk with the other volunteers…it seems like many people tend to return to the same activities again and again.

For what it’s worth, there are 3 types of activities I choose from: something outside, working in a soup kitchen/food support, or directly working with other people.

Outdoor stuff

The outdoor activities are things like working in a community garden, park, or urban farm. These are definitely more spring, summer, and fall activities. Usually we’re weeding, pruning, or some other type of working with your hands in nature activity. I learned at some point that humans find gardening extremely satisfying, so I try signing up when I can.

Volunteering at an urban farm in the Bronx, for International Rescue Committee

Food stuff

The food support/soup kitchen activities are related to feeding people. It might be meal prepping, which could be as simple as making sandwiches or as complicated as cutting up raw chicken. I have also delivered prepared meals and packed fresh produce to be given away. Once I signed up at a church where they cooked and passed out food that day, so everyone was really rushing. But typically I’m doing prep for a future meal and it’s not too crazy.

People stuff

The direct service activities are those where you’re working directly with the people who benefit, like seniors, the disabled, or kids and their parents. It can be the most fulfilling but also the most emotionally taxing. I recently signed up for a seniors-focused activity. I was nervous and didn’t know what to expect. I considered dropping out. But I stuck with it and it turned out better than I expected. I’ll write about some of what I’ve learned with that in a later post.

In summary, volunteering can provide opportunities to explore your city, try a new activity, and find new interests. Maybe try something you haven’t tried before — like meeting some fancy chickens! 🐔

I’ve been regularly volunteering and I’ve decided to share some of the not so obvious benefits. Two reasons I’m sharing in this post are improving small talk and practicing punctuality.

Introduction

I have really been remiss in updating this blog. I have about 7 draft blog posts that I’ve started and just haven’t come back to. In one of them, I have something like, “Time has been really relative since 2020.” Ain’t it the truth!

Well, one thing about this blog is that I’ve really moved away from blogging about tech, which was one of the original purposes of this blog. Actually, a big reason was to document projects for a Master’s program. But lately, I’ve found more interest and joy in writing about things related to the arts and culture, and my life in general: movies, museums, etc.

For this post, I wanted to write about something that has become a regular part of my life: volunteering, which I started doing a lot last year.

When I talk about it with other people, they typically say something like, “That’s great!” But truthfully, down inside, I always cringe a little bit. Not because they aren’t right. Volunteering is great — but sometimes I feel like my motivations for volunteering aren’t really all that generous and altruistic. In fact, sometimes they feel a bit selfish.

I’ve been thinking a little bit about the reasons I volunteer and what I get out of it. I decided to list some of the not so obvious reasons that volunteering provides that aren’t just doing nice things for other people. (I will share some obvious reasons, eventually!)

I initially planned to share all of my reasons all at once, but I’ve found that with more to write about, there are more opportunities to re-read and edit. This just delays publishing. So I’ve decided to share them one at time, or maybe more, so I can think about each part in more depth.

Joys of volunteering: reasons 1 – 2

Reason 1: Improve your small talk

Most of the time when I volunteer, it’s with people I’ve never met and often won’t meet again. Each project or session date is about 2-4 hours. I find it’s much more pleasant to introduce myself and get to quickly know the people I’ll be working with than to keep quiet and not say anything to anyone.

The most common topic we often talk about is asking each other if we’ve participated in the activity before. If the activity is outside, we might talk about the weather. Once, another participant had a T-shirt with a well-known logo, so I asked her about her shirt. Another person might mention their spouse, kids, pets, or their neighborhood and that leads to conversation. Or maybe we comment on the work itself.

Sometimes, the activity involves serving other people, like working with seniors or kids. This is also another chance to talk with people who are different from you and find ways to connect. I’ve learned that seniors and the differently abled are really the same as everyone else, but the way they express themselves is different because of their cognitive or physical differences.

Repeatedly volunteering has been a really good way to practice small talk and learn how to break the ice. I feel more comfortable making small talk now than before.

Reason 2: Practice punctuality

I am a card-carrying tidsoptimist. This means I tend to overestimate how much time I have or underestimate how much time a task takes, so it can lead to lateness or maybe a task takes longer to complete than I initially estimated.

Although my time optimism is in my nature, its not good to be late all the time, especially when meeting with other people. I made it a point in 2023 and in 2024 to focus on my punctuality. Not only to improve how others saw me, but also to shut up that voice in my head that berates me for being late all the time.

Part of my solution for this has been to make early morning doctor or dentist appointments and volunteer for activities that start early. It’s been an excellent motivator for me because…who wants to be late to a soup kitchen?

I’m someone who signs up for different activities vs picking the same one over and over, so the volunteer activities have occurred all over the city. Sometimes more than an hour away. I’ve learned to plan ahead by actually mapping out the route ahead of time rather than assume I know the route. So far, my plan is working. I recently joined a volunteer activity that had an 8:45 AM start time!

And I made it. Go me! Here’s a nice photo from that day.

Tree blossoms on Governor’s Island, the location of a recent volunteer activity that started at 8:45 AM.

In summary, reasons 1 and 2 are improving small talk and practicing punctuality. Check back again for additional reasons to volunteer and, if you’re so motivated, get out there and volunteer!

In Arlan Hamilton’s book, “It’s About Damn Time”, she shares a list of 17 songs that help her feel empowered.

I was recently reading Arlan Hamilton’s book, It’s About Damn Time: How to Turn Being Underestimated Into Your Greatest Advantage. In Chapter 2, Part 6, she included tips she’s found helpful when she’s about to give a speech or a talk. The tips are to help combat imposter syndrome and other normal feelings of insecurity. Her first tip 1 is to listen to songs of empowerment and she shared her list of songs. I decided to write the list down and give the songs a listen, and see if her songs empowered me.

Rather than hunt down audio tracks, I searched YouTube and created the list below.

Well, I don’t know how empowered I feel after this list, but I still think this is a great exercise. I should come up with my own list and see what I can create. It would be nice to have a list to listen to before work or any time I want to feel a little push.

There’s more to be found about Arlan Hamilton, her book, and her venture capital firm, Backstage Capital, at itsaboutdamntime.com.

From January 12-25, 2022, The Jewish Museum and Film at Lincoln Center are delighted to continue their partnership to bring you the 31st annual New York Jewish Film Festival, presenting films from around the world that explore the Jewish experience.

Thanks to the magic of the internet, I got to attend this festival online for the first time. Thanks to work schedules and whatnot, I only watched 3 films. Despite my love of film festivals, yet limited film viewing, I was quite impressed with how many films, and even TV shows, there were to experience.

One thing I neglected to do was watch and pay attention to all of the Q&As. Usually Q&As follow film screenings, when they’re held in person, so all you have to do is remain in your seat. This time, I was just happy I was able to make time to watch the films.

Anyway, here are the 3 films I watched, in the order I watched them, plus some additional thoughts and details about the films.

With No Land (2021)

In May 1991, 15,000 Ethiopian Jews were airlifted to Israel in less than 24 hours’ time. Known as Operation Solomon, this covert mission coordinated by the Israeli military saw the birth of eight babies en route and set the world record for the most passengers on a single aircraft. History regards the endeavor as an unqualified triumph, but 30 years later, the full story is being told. Aalam-Warqe and Kobi Davidian delve into the details that have been suppressed for all this time, and explore the desperate but motivated measures taken by Jewish Ethiopian activists in Israel, North America, and their country of origin. Archival footage and firsthand accounts of participants lend nuance to a story heretofore viewed as black and white, supplemented by accounts of recent efforts to finally relocate to Israel those whom Operation Solomon left behind.

I’m not sure I knew much about the history of these events prior to watching the film. Although the summary of the film is about the 1991 airlift, much of the film goes into events that happened prior to that — about the Ethiopian Jews who had been allowed into Israel earlier than 1991, how families were split up, how some were reunited — and how Israel refused to accept Ethiopians despite their religion.

There was also a historical account of the political and military situation within Ethiopia, and how other countries and NGOs explicitly or secretly cooperated with the plans to relocate Jewish Ethiopians. Some had fled to Sudan while others remaining in Ethiopia were stuck between two fighting contingents — which seem to have renewed their conflict recently, again, if it ever went away.

But a very interesting film and I’m glad I learned more about it. There is definitely more information about Operation Solomon to be found online.

Click through to watch the first-hand account from someone who, at age 11, was airlifted out of Ethiopia as part of Operation Solomon. The witness describes his experience, and also talks about issues of assimilation between his and his parents’ generation.

Cinema Sabaya (2021)

Nine women of divergent backgrounds enroll in a video production seminar that promises to teach the fundamentals of filmmaking. These residents of Hadera, Israel are Jewish and Arab, observant and secular, ensconced in all manner of domestic arrangements, with life spread out before some of them and regarded by others in hindsight. Strangers to one another (one of the Jewish attendees has never interacted with Arabs until now), the students share the common goal of self-expression through their cameras, with Tel Aviv–based filmmaker Rona (Dana Ivgy, acclaimed star of Or and Zero Motivation) supplying instruction. Orit Fouks Rotem casts her debut feature with a mix of seasoned and nonprofessional actors, all shooting their own footage and viewing their colleagues’ work for the first time on screen. Sparked by former workshop leader Rotem’s personal experiences, Cinema Sabaya presents a deft and never didactic portrait of art’s capacity to unite disparate communities.

Cinema Sabaya, clip (2:21) Other Israeli Film Festival (The official trailer is Unlisted on YouTube.)

The description seems provocative, like maybe this will be a story about Arabs and Israelis. Instead, the story was much more about the lives of the women, how free they felt at expressing themselves, and the support they gave each other while revealing sensitive aspects of their lives.

For instance, one of the Israeli women seems at first grating and displays, maybe, this “toxic positivity” I’ve been reading about. She seems overly positive, very smiling…until she reveals that she hasn’t really interacted with an Arab person. She said, during the suicide bombings in Israel (before the wall), she crossed the street whenever she saw an Arab person. Later, during the course of sharing her filming assignments, it turns out her home life is not as positive as she appears to be. Her husband is withdrawn, likely suffering from PTSD. Her daughter doesn’t want to engage with her, and so forth.

Another woman tells the group she has had to move herself and her children back in with her mother after leaving her husband. Her dream is to buy an apartment. During one of her video assignments, it’s revealed that she and her kids are living in a single bedroom with all the stuff she was able to grab when she quickly left her husband. It’s a very crowded and cramped room, and clearly not a place where she or her children can thrive.

In another instance, a Muslim Arab woman, with 6 children, shares her dream of getting a driver’s license so that she doesn’t have to rely on her husband so much. Later in the film, the group role plays and acts out scenes where they pretend they’re confronting someone in their life about whatever dream they have. This woman plays herself and another woman plays her husband, and seems to accurately portray his dominant role in their marriage and her life. The Muslim Arab woman essentially gives up the argument when her partner declares, role-playing her husband, that he has decided she doesn’t need a license and he’s made up “his” mind. The rest of the group tries to encourage her to continue and just pretend, and to say what she feels even if she wouldn’t say it in real life. In a cathartic moment, she reveals that she regrets ever meeting her husband or marrying him at all. She reveals that she hates that he touches her, hinting at sexual aggression within the marriage. It’s clear she holds in her feelings of contempt for her husband. When the other woman tries to push her a little bit, to “give her courage”, the Muslim Arab loses her composure and attacks the woman by pushing her down, and then runs out of their community center. She disappears for the next few sessions, only to reappear on the day when they receive their completion certificates.

I felt it was a very interesting story about the motivations and, not spectacular, but plain dreams of women, and how their wants are withheld or thwarted often by the men in their lives or by expectations for women to support or be the center of the family.

Shtetlers (2020)

An invaluable record of tight-knit communities that endured genocide and shifting political regimes, Shtetlers offers a glimpse at the small Jewish towns (“shtetls”) dotting the former Soviet Union—towns where for many years Yiddish continued to be spoken and ancient rituals dutifully observed. Located on the fringes of the territory, in what are now Ukraine and Moldova, these villages that withstood the Holocaust managed to abide by supplying non-Jewish neighboring towns with goods and services. Director Katya Ustinova examines nine former shtetl inhabitants, now spread out across the world, and solicits their memories of a resilient but ultimately vanishing way of life. Ustinova’s documentary serves as an elegy for these once numerous strongholds of tradition and culture, but also, by archiving the recollections of those who experienced them firsthand, preserves them.

For this film, I did watch the Q&A, because I started writing this before the film expired for my account. And I got to hear a little more about the background of the film. Sadly, I learned everyone in the film has passed away, except for one person. (Most of the people were elderly and I believe it some of the footage goes back to 2015.)

On a positive note, the director revealed that there was Instagram account for the film, with additional animations and video not used in the film, so there’s more film to explore.

As I mentioned above, it was my first time participating in this film festival. I think Film at Lincoln Center tends to host many types of film festivals, so I’ll try to pay more attention from now on.

There seemed to be something like 30 films, both online and in-person. The festival must have been fairly popular because many of the online films sold out or expired before I could watch them.

The line-up of online films seemed like a really nice mix. For instance, they had at least one option of short films (“Shorts”), which I often enjoy, but I didn’t watch any this time.

Anyway, definitely recommend watching any of the three films above, if the chance arises. In the meantime, I’ll take note for next year’s festival and onward to the next!

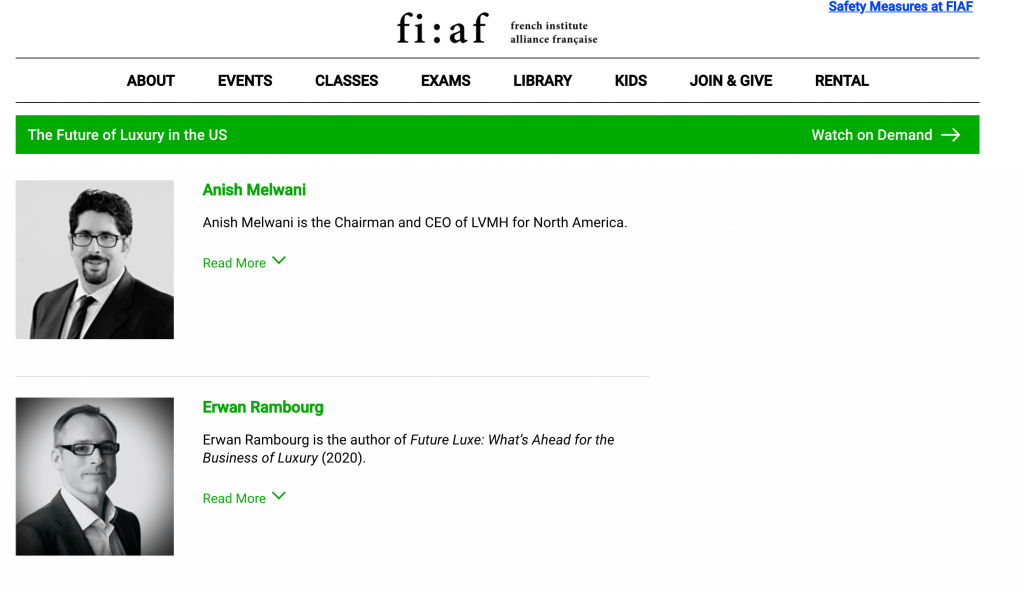

Title: Breakfast with Anish Melwani, Chairman & CEO of LVMH Inc (North America), In Conversation with Author Erwan Rambourg

Date: Wednesday, November 3, 2021

Description: In a thought-provoking conversation with author Erwan Rambourg (Future Luxe: What’s Ahead for the Business of Luxury, 2020), Anish Melwani will discuss the ever-increasing demand for iconic luxury goods in the United States.

Speakers:

FIAF biography overview for Anish Melwani, Chairmain and CEO of LVMH for North America, and Erwan Rambourg, the author of Future Luxe: What’s Ahead for the Business of Luxury (2020).

Discussion

In the early part of the talk, Melwani talked about his own background. Prior to his role at LVMH, he admitted he had not worked in luxury/prestige previously.

On creativity: He talked about his first meeting with Marc Jacobs (the actual person), and being blown away by the creativity he witnessed. He said compared to his previous experience at McKinsey, the creativity at LVMH was off the charts.

On the state of Luxury in North America: More customers are now shopping from home, leading to more access to shopping in smaller markets.

On the organization of LVMH: LVMH is decentralized, focused on Maisons (houses). That’s what makes it work — or it works despite these “inefficiencies”.

Creativity and competition at LVMH: Each Maison competes with each other to drive innovation and creativity. That’s what compensates for “inefficiencies”. From a conglomerate perspective, it would make more sense to consolidate the Maisons. But from a creative perspective, it doesn’t.

Was anything missing from LVMH? The interviewer or someone in the crowd asked if LVMH was missing anything. I don’t recall how this question ended in an answer on cosmetics or skincare, but I learned that LVMH owns Fenty skincare and Fresh. He talked about the wines and spirits division (perhaps in the context of recent acquisitions). And he mentioned that LVMH had acquired hotels and other properties via Belmond.

Fenty: A few points

Prior to this event, I did not know Fenty was part of LVMH.

He mentioned the fact that Fenty debuted with 40 shades of foundation, which was completely unheard of at the time due to being inefficient from a sales perspective because some shades sell out more than others. However, although this is the case, the point, he said, was to show the customer that they were seen (emphasis mine).

He also shared a comment from one of Rihanna’s Savage X Fenty shows — something about how customers can really see themselves on the stage/

The visibility, he said, is what leads to the idea of prestige. (Or something like that.)

Fenty came out of Kendo, an incubator in LA, specific to Sephora.

Fenty does well in the US, which is more diverse compared to Europe.

Personal side note regarding Fenty: Although they may have released 40 shades, and many of those shades don’t sell as well as others, I have had much difficulty finding foundation shades in my skin color — foryears. Colors are either too red/orange, too dark, too light…if they exist at all. They recently released a new product, Eaze Drop, a blurring skin tint. It’s extremely popular. My shade, #10, has been out of stock for MONTHS. It seems to me there is some business sense in creating these in-between shades.

As he correctly mentioned, an NFT is an address on a blockchain.

Events & Experiences

There is a high-demand for events, and demand for experiences is increasing. But what he’s not sure of is if there will be larger events in big cities, or many smaller events.

Using digital can help spread the experience around, which is kind of the traditional model. But he’s not sure what the model will be in the future, given technical advances and demand, etc.

My Questions

As I was watching online, I wasn’t able to ask questions directly. The online viewers weren’t encouraged to add questions to the Zoom Q&A. But if I had been given the opportunity to ask questions, I would’ve asked this:

Leather/Fur: Seems like attitudes are changing about fur and meat, of which leather is a by-product. Any thoughts about that?

2nd-Hand Market: I didn’t have a specific question, but I was generally curious about the 2nd-hand market.

Final Thoughts

This was a really well-done, live online event. I didn’t get screenshots, but below each presenter were names and titles to describe what they did. It was really professional.

The only downside was sometimes when audience members would stand and ask questions, they sometimes begin speaking before getting the microphone. This happens at almost every event, with audience goers believing that since the people presenting and those around can hear them, the microphone picking up the event can also hear them. It cannot. Thankfully, FIAF corrected this very quickly right after one person began speaking.

I hope they produce more webinars like this again. Part of why I could not attend is because it was at 8:30AM, which is too inconvenient for me to go to and return home in time for work. Also, 8:30AM is pretty early. 🙂

Anyway, it was informative, produced very well, and very worthy of my time. I hope they do more morning series like these.